⚠ FRAUD ALERT:

Platinum Management has been made aware of fraudulent rental scams involving unauthorized individuals impersonating our company.

Learn More

⚠ FRAUD ALERT

Platinum Management has been made aware of fraudulent rental scams involving unauthorized individuals impersonating our company and advertising properties online.

NEVER send money, deposits, application fees, gift cards, wire transfers,

Zelle payments, Cash App payments, or any other funds without first verifying

the property and representative directly with Platinum Management.

If you have any concerns regarding a listing or communication you received,

please contact us immediately at

(517) 698-8409 or

[email protected].

Platinum Management is not responsible for payments made to unauthorized third parties.

For a brief moment, it looked like U.S. homebuyers would finally catch a break.

The housing market was beginning to thaw as mortgage rates fell in September to a two-year low. But in the past few weeks, borrowing costs have surged, by one measure even crossing 7% and raising questions about whether a fledgling recovery in home sales contracts will persist.

On Thursday, Freddie Mac reported that the average rate on a 30-year mortgage in the U.S. rose for the fifth straight week, returning to its highest level since early August.

It’s a tricky time for whipsawed home shoppers with the market taking yet another twist. And it’s unclear exactly how many buyers will try to fight through affordability challenges to land a deal before lower rates that are expected next year lure in more competition.

One measure of demand — weekly mortgage applications — fell throughout much of October as borrowing costs climbed, but ticked up in the week ended Oct. 25, according to Mortgage Bankers Association data.

The Federal Reserve, which cut its interest rate in September for the first time in more than four years, is scheduled to meet next week, after the presidential election Nov. 5. Yields on 10-year Treasuries have risen since the central bank’s last meeting in part because strong economic data has cast doubt on the likelihood of deep cuts ahead.

The average rate on a 30-year mortgage in the U.S. rose to 6.72% from 6.54% last week, mortgage buyer Freddie Mac said Thursday. That’s still down from a year ago, when the rate averaged 7.76%.

Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners seeking to refinance their home loan to a lower rate, also increased this week. The average rate rose to 5.99% from 5.71% last week. A year ago, it averaged 7.03%, Freddie Mac said.

The jump in rates serves as a double whammy for homebuyers, choking off affordability and discouraging more owners from listing properties. The supply of housing has been kept tight by the so-called lock-in effect. Few homeowners are willing to sell if it means taking on a higher mortgage rate.

“It’s going to put a damper on sales — affordability has gone down and the lock-in effect has increased,” said Scott Buchta, head of fixed income strategy for Brean Capital. “We think we’ll need a sub-5.5% mortgage rate to unthaw the housing market, which probably doesn’t happen any time soon unless we go into a recession.”

Even a modest drop in borrowing costs could help the market pick up, said Ralph McLaughlin, senior economist at Realtor.com. When rates fell to around 6% in September, for example, it attracted buyers who eventually signed contracts to purchase homes this month. Pending sales in October were up nearly 10% from a year earlier, according to Realtor.com data.

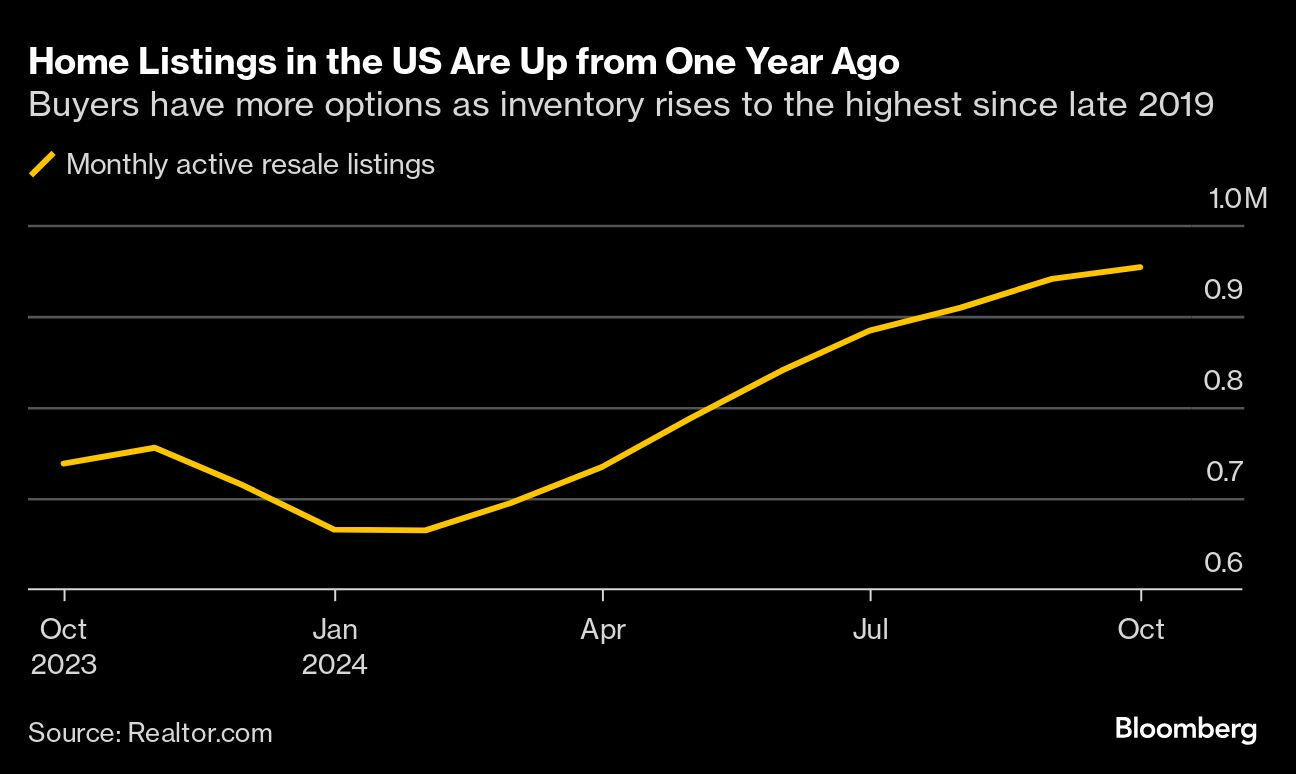

If rates stay high, demand will likely pull back, according to McLaughlin. But for buyers who aren’t priced out of the market, it’s actually a good time to snap up a property, he said. Inventory in October, made up of homes for sale that didn’t find buyers in the summer along with a growing number of new listings, jumped to the highest since December 2019, according to Realtor.com data.

The higher inventory is helping give buyers more leverage over sellers, according to David Lampe, an agent with the Principal Team at Metro Brokers that’s helping Zamora. “I’m seeing a ton of homes that are overpriced, and you’re seeing multiple price reductions,” Lampe said.

But some house hunters are having to consider smaller properties or fixer-uppers because high borrowing costs are shrinking their budgets, he said.

“There was a lot of excitement in July, August and September as rates were coming down,” said mortgage banker Shant Banosian in Waltham, Mass. “When rates start approaching 7%, it changes peoples’ budgets big time.”