Mortgage companies get big boost as owners tap into surging home equity

The significant inflation throughout the U.S. economy of the last several years has undoubtedly brought harm to American consumers. But it’s also resulted in massive appreciation for home values.

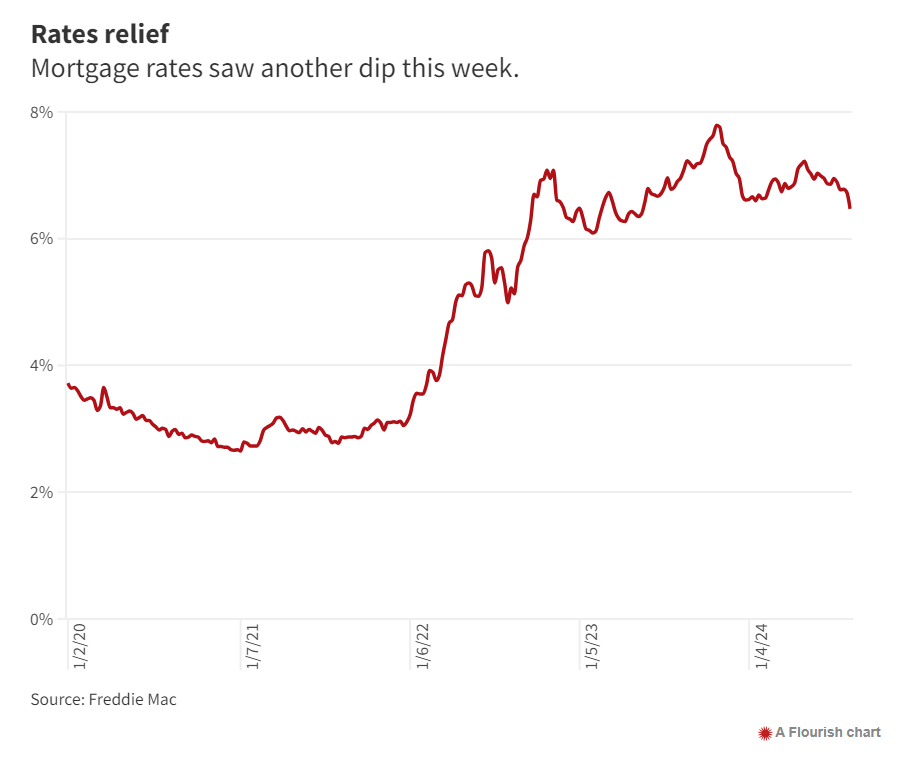

That second factor, given that interest rates have more than doubled since the summer of 2021, means many homeowners locked into low rates are tapping into the appreciation of equity in their homes, often just to stay afloat given increasing credit card debt and other financial challenges.

“People have a lot of equity in their home, but no money in the bank,” Joe Fuca, a mortgage broker with Simple Home Lending in Macomb Township, said of what he’s seeing as the key driver for the rise in home equity lines of credit, or HELOC loans. Around 80% of the home equity loans Fuca works on, he said, are for someone who needs the money for general financial purposes as opposed to funding a home repair or other specific needs, as has been a traditional reason.

Brokers like Fuca and other executives in housing finance say the popularity of home equity loans has increased in recent years with a key advantage being that they effectively act as a second mortgage, giving borrowers access to cash while allowing them to keep the low interest rate on their primary mortgage.

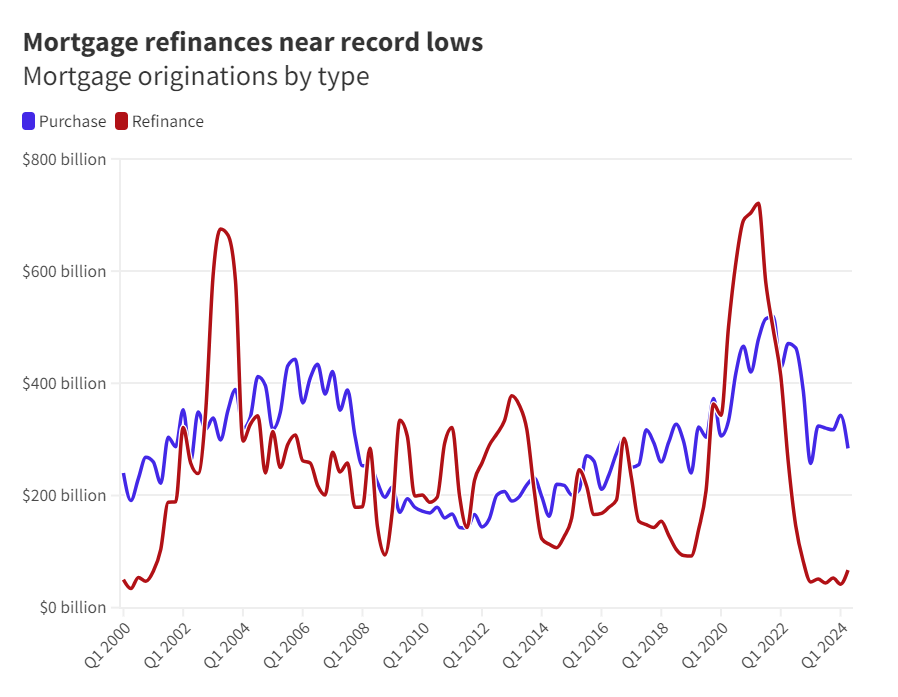

Given that most homeowners at present have a relatively low interest rate from the COVID-19 pandemic era, a cash-out refinance loan would be “financially devastating” for many borrowers as their monthly payment would skyrocket, Fuca said.

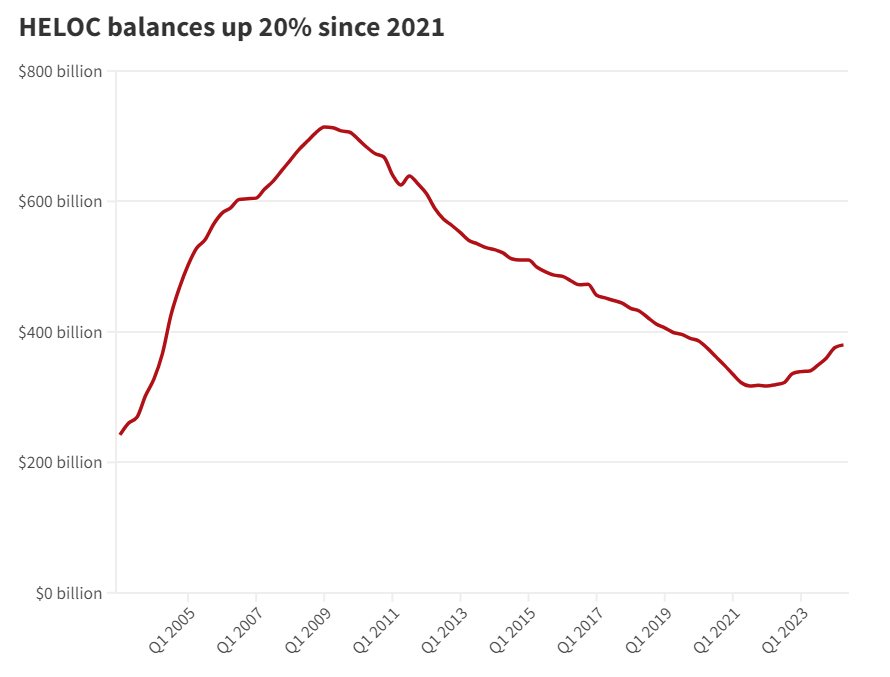

Home equity borrowing petered out during the pandemic years when interest rates were low and homeowners opted to refinance and paid off debt as government money was flowing. But HELOCs have picked up again as interest rates climbed, household debt has soared and home values appreciated.

Such loans bottomed out at the end of 2021 but have rebounded in recent months. In the second quarter of this year, Americans tapped about $380 billion in home equity value, the highest since early 2020, according to data from the Federal Reserve Bank of New York’s Credit Panel and Equifax.

“Given record levels of home equity and the undesirability of cash-out refinancing, one may actually wonder why we are not seeing a larger surge in HELOC originations,” New York Fed researchers wrote in a recent post.

At Rocket Companies Inc., the Detroit-based parent of Rocket Mortgage, the company offers a home equity loan product more comparable to a personal loan, as opposed to traditional HELOCs, which function more as a line of credit, similar to a credit card.

Rocket’s home equity loan product reached an all-time high in the second quarter, more than doubling from a year ago, according to CEO Varun Krishna. The company does not break out specific volume on such lending.

During the second quarter, Rocket launched an Automated Valuation Model, which allows for a “digital alternative” to more traditional in-person home appraisals. It allows for delivery of cash to borrowers in as little as one week, according to the Rocket earnings report.

“This is a great example of product market fit,” Krishna said of home equity loans during an earnings call with analysts and investors earlier this month. “And we’ve seen strong demand in the product volume … because it’s an offering that’s incredibly valuable to our clients.”

Likewise, Pontiac-based United Wholesale Mortgage Corp. — currently the nation’s largest mortgage lender — does “thousands” of home equity loans every quarter, according to UWM Chief Strategy Officer Alex Elezaj.

Like most other financial products, home equity loans are largely a function of the broader economic climate, Elezaj noted. During the pandemic, even when usage was lower than today, such loans were often used to fund home improvements while at present they’re often used to pay down debt that Americans have built up.

The loans have the advantage of generally carrying a lower interest rate than traditional credit card debt. They are also a strong product for more traditional banks and bring in a “steady volume” of business, according to Joe Batt-Capps, vice president of home equity and loan innovation for Grand Rapids-based Lake Michigan Credit Union, the state’s largest credit union.

“This can be attributed to the rise of home values in the market, which has allowed our members to leverage that equity at a low interest rate,” Batt-Capps wrote in an email to Crain’s. “Many of our members are choosing to invest in their current homes or improve their financial standing by consolidating high interest credit card debt.”

In recent months, and increasingly the last week or so, talk has turned to lower mortgage interest rates. Mortgage rates last week hit their lowest point in more than a year.

Given the apparent change, it would seem likely that demand for home equity loans could soften once more in the coming months, Elezaj said.

“Obviously, the lower the rates go, people aren’t as concerned about getting a HELOC,” Elezaj told Crain’s. “They’re in the money to refinance their loan. Anybody who’s gotten a 30-year fixed loan in the last two years … there’s a huge opportunity for them to save money (on) mortgage rates.”